You mine some Bitcoin, watch the wallet fill up, feel pretty good about it. Then someone asks whether you’ve set aside money for taxes. That’s when things get uncomfortable.

Crypto mining income is taxable in the US. The IRS settled that question back in 2014 and hasn’t deviated since. But the how depends on whether you’re running rigs as a business or mining occasionally on the side, what you did with those coins after you received them, and whether you tracked fair market value on the day they arrived. Get those details wrong and you’re either overpaying or setting yourself up for a compliance problem down the line.

This guide covers exactly what the IRS expects and how to stay on the right side of it.

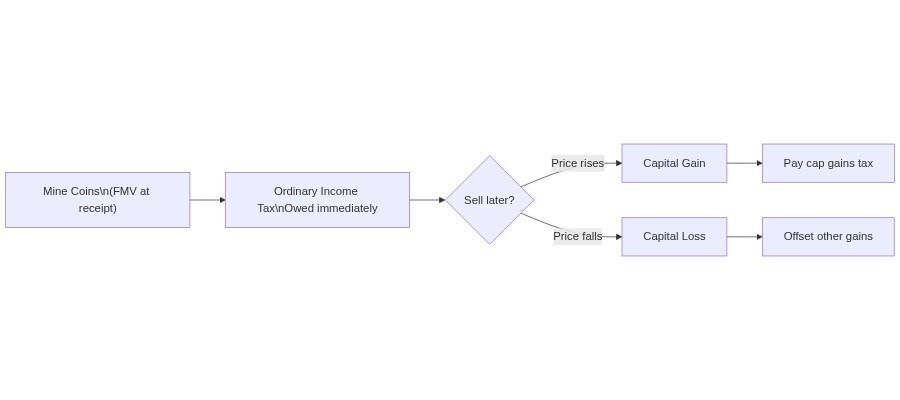

Mined crypto is taxable as ordinary income at the moment you receive it, valued at fair market value in USD on that date. When you eventually sell, you pay capital gains tax on any appreciation. Business miners can deduct electricity, hardware, and operating costs. Hobby miners can’t deduct a thing. The distinction matters — a lot.

Is Mining Income Taxable? (Short Answer: Yes)

Yes, mining income is taxable. The IRS established this definitively in Notice 2014-21, ruling that cryptocurrency received through mining is gross income at its fair market value on the date of receipt. That income is treated as ordinary income — not capital gains — at whatever tax bracket applies to your total income for the year. (IRS Notice 2014-21, 2014)

We’ve seen this trip up miners repeatedly. The assumption — “it’s crypto, not really income until I cash out” — doesn’t hold. From the IRS’s perspective, receiving mined coins is economically identical to receiving payment for a service. The wallet fills up; the tax clock starts.

The follow-up question is whether you’re mining as a hobby or a business, which determines which forms you file and whether you can deduct any costs against that income.

How Does Crypto Mining Tax Work?

Mining creates two separate taxable events. Most people know about one; the second catches them off guard.

Income Tax When You Receive Mining Rewards

The first taxable event happens the moment new coins arrive in your wallet. You owe ordinary income tax on the fair market value (FMV) of those coins in USD at the time of receipt. It doesn’t matter whether you sell immediately or hold for years. The income event already happened.

Say you mine 0.1 BTC when Bitcoin is trading at $90,000. That’s $9,000 of ordinary income, recognized right now. Your cost basis in those coins is $9,000.

This mechanic is what creates liquidity problems. You’ve earned income on paper, in a volatile asset that might drop 40% before you’ve converted enough to pay the bill. Anyone who mined in late 2021 and held through 2022 knows this feeling: they owed taxes on coins worth far less come filing time.

Capital Gains Tax When You Sell

The second taxable event happens when you dispose of the coins: sell, trade, or spend them. You calculate the gain or loss against your original cost basis (the FMV when you received them from mining).

Using the same example: if you sell that 0.1 BTC later for $11,000, you’ve got a $2,000 capital gain. If it’s fallen to $7,000, you have a $2,000 capital loss. The holding period determines the rate:

- Short-term (held less than a year): taxed at ordinary income rates, same as the mining income itself

- Long-term (held over a year): preferential rates of 0%, 15%, or 20% depending on your income

That’s why many miners deliberately hold mined coins for at least 12 months before selling, converting what would be ordinary income tax on a gain into a much lower long-term capital gains rate.

What’s the Crypto Mining Tax Rate?

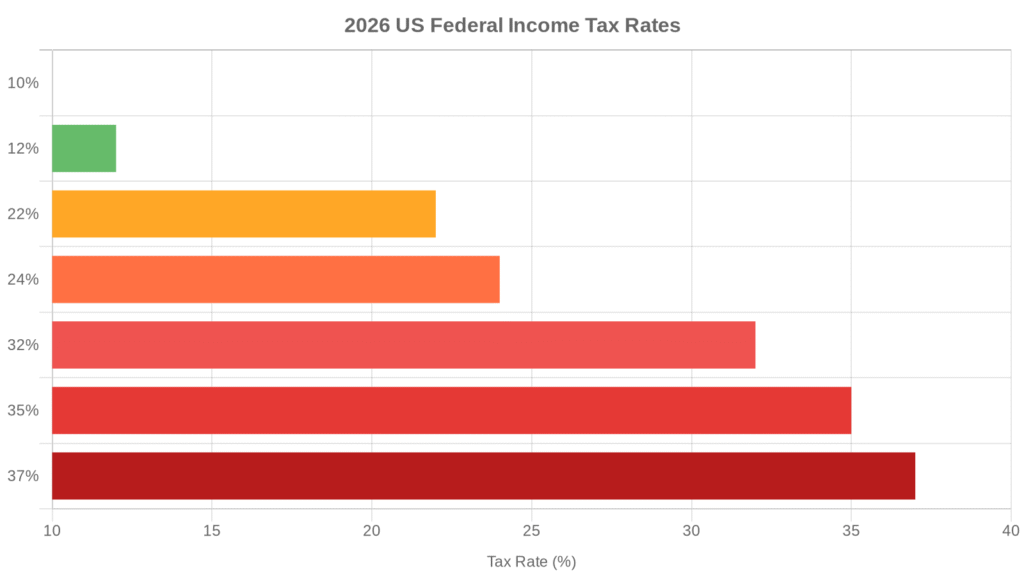

Mining rewards are taxed at ordinary income rates — 10% to 37% depending on your total taxable income and filing status. For 2026, the top 37% bracket starts at $640,600 for single filers. Most miners fall somewhere in the 22-32% range. (IRS Revenue Procedure 2025-32, 2025)

Here’s the part people miss: sole-proprietor business miners also owe self-employment tax on top of income tax. Self-employment tax runs 15.3% (12.4% Social Security, 2.9% Medicare). Put a 22% income tax bracket on top of 15.3% SE tax and you’re looking at an effective rate of 37% on net mining profits before any deductions. That gets people’s attention.

Business miners who incorporate can structure compensation to reduce SE tax exposure. That’s a conversation for a crypto-specific CPA, not a tax guide.

Long-term capital gains rates when you eventually sell mined coins are 0% for taxable income under $49,450 (single filers, 2026), 15% for most filers, and 20% for the top bracket. The gap between ordinary income rates and long-term cap gains rates is often 10-22 percentage points. That differential is why the hold decision matters so much.

Hobby Mining vs. Business Mining: Why the Distinction Costs Miners Thousands

This is the most consequential classification in crypto mining tax. The IRS doesn’t make it simple, but the stakes are real.

The IRS evaluates nine factors to classify an activity as a business or hobby, weighing profit motive, time and effort invested, reliance on income, and track record of profitability. No single factor is decisive. In practice: if you’re mining regularly with dedicated hardware, tracking operational costs, and genuinely trying to profit, you’re probably running a business.

Why does it matter?

Hobby miners report mining income as “Other Income” on Schedule 1 of Form 1040. No deductions. At all. The Tax Cuts and Jobs Act of 2017 suspended the miscellaneous itemized deductions that used to let hobby miners write off some expenses. So hobby miners report gross income and pay full ordinary tax on it. Electricity bills, hardware depreciation, pool fees: none of it offsets anything.

Business miners file on Schedule C. They can deduct all ordinary and necessary business expenses, which for a meaningful mining operation can dramatically reduce taxable income. We’ve looked at setups where gross mining revenue of $180,000 came down to $40,000 in net taxable profit after legitimate deductions. Electricity alone was $80,000. That’s the kind of difference that pays for an accountant many times over.

The tradeoff is self-employment tax: business miners pay 15.3% SE tax on net profits; hobby miners don’t. But for most operations with real costs, the deductions more than offset the SE tax hit.

What Expenses Can Business Miners Deduct?

If you qualify as a business miner, these expenses are generally deductible as ordinary and necessary costs:

Electricity. The dominant expense for most miners, and fully deductible. Keep actual bills with usage dates. Home miners can only deduct the portion specifically attributable to mining, not your entire household power bill.

Mining hardware. GPUs, ASICs, cooling systems, and related equipment. You can depreciate over the asset’s useful life or take a Section 179 deduction for the full cost in the purchase year (the 2026 Section 179 limit is $1,220,000). Bonus depreciation rules may also apply depending on current legislation.

Pool fees. This one slips through the cracks constantly. Most miners join pools and pay fees that run 1-3% of mining rewards. Those fees are deductible business expenses. Track what actually hits your wallet (net of pool fees) rather than reporting the gross payout figure the pool calculates before deductions.

From what we see in the mining community, pool fees are the expense category that trips people up most. Miners report the gross reward figure as income without accounting for what the pool already took out. Small percentage, but across a year of regular mining it adds up. It’s a legitimate deduction they’re leaving on the table.

Rented space. If you rent a warehouse, colocation facility, or dedicated space for your rigs, that cost is deductible. Home miners can claim a home office deduction for the portion of their home used exclusively for mining.

Repairs and maintenance. Replacing dead GPUs, fixing cooling systems, maintenance contracts. Standard business expense treatment.

Internet and software. Business-use portions of your internet connection, any mining management or monitoring software.

One area that gets complicated: cloud mining contracts. Whether you receive tokens from a cloud mining provider or whether you’re purchasing a service from them affects income and expense characterization differently. At scale, this warrants professional advice.

How to Pay Tax on Mined Crypto

The mechanics aren’t complicated once you understand the sequence.

Record FMV at every receipt event. Every time mining rewards arrive in your wallet, note the date, amount received, and USD value at that moment. Most major exchanges and wallets track this historically; you can also pull prices from CoinGecko or CoinMarketCap for any date. This number is both your taxable income and your cost basis.

Disposals need a separate ledger. When you sell, trade, or spend mined coins, record the date, sale price, and original cost basis. The difference is your capital gain or loss for that disposal event. A spreadsheet or a crypto tax software account handles this automatically if you sync your wallets.

Accounting method selection matters more than most miners realize. The IRS allows FIFO (first-in, first-out), HIFO (highest-in, first-out), or specific identification. HIFO typically minimizes gains by selling the highest-cost-basis coins first, which helps in a rising market. Revenue Procedure 2024-28, effective January 1, 2025, gave taxpayers more flexibility to allocate unused basis to remaining digital asset positions, which changed the optimization math for miners who’ve been accumulating across multiple tax years.

The right forms depend on your classification.

- Hobby miners → Schedule 1, Line 8z (“Other Income”)

- Business miners → Schedule C for income and expenses; Schedule SE for self-employment tax

- Everyone who sold mined coins during the year → Form 8949 and Schedule D for capital gains/losses

From 2025 onward, expect Form 1099-DA from custodial brokers for any digital asset sales conducted through centralized exchanges. If you’ve been selling mined coins through a CEX, that form will now document the transaction. Note: 1099-DA covers the sale, not the original mining income event itself; the mining receipt remains self-reported.

Keep records for at least six years. Standard IRS audit window is three years, but that extends to six if the IRS suspects substantial underreporting (defined as underreporting 25%+ of gross income). Blockchain transactions are permanent and public. They’re not going away.

Do You Have to Pay Quarterly Taxes on Mining?

Probably yes, if mining generates meaningful income.

The IRS requires quarterly estimated tax payments when you expect to owe more than $1,000 for the year and your withholding won’t cover at least 90% of your tax liability. Mining income has zero automatic withholding, which puts almost every active miner squarely into the quarterly payment requirement. (IRS Publication 505, 2026)

2026 quarterly deadlines: April 15, June 16, September 15, January 15 (2027).

Estimating is genuinely hard when your mining revenue swings with difficulty adjustments and coin price. A practical approach many miners use: set aside 25-35% of each mining reward as it arrives (higher if you’re in the 32%+ bracket or owe SE tax), then reconcile at year-end. It’s not precise, but it keeps you from facing a large underpayment penalty plus an unexpected bill on coins that have since dropped in value.

What’s the Proposed 30% Crypto Mining Excise Tax?

The short version: it was proposed, it failed, it’s not currently law.

The Biden administration introduced the Digital Asset Mining Energy (DAME) excise tax in 2023: a proposal that would have imposed a 30% tax on the electricity costs of crypto mining operations, staged in over three years (10% in 2024, 20% in 2025, 30% in 2026). The stated rationale was environmental externalities: carbon footprint, local energy price impacts, grid strain. The proposal appeared in the 2024 and 2025 budget submissions.

Neither version passed. The 2023 version was explicitly dropped from the debt ceiling negotiations in May of that year. (Fortune Crypto, May 2023)

As of April 2026, there is no 30% excise tax on crypto mining in US law. The current political environment is meaningfully more crypto-friendly than 2023, and the appetite for a mining-specific energy tax has cooled significantly. That said, legislative situations evolve. Miners making long-horizon infrastructure decisions should watch regulatory developments through industry publications and Congressional tracking services.

What does apply right now: ordinary income tax on rewards, self-employment tax for sole proprietors, and capital gains tax on disposals. For serious operations, that already produces effective rates in the 30-40%+ range without any additional excise layer.

The Bottom Line on Crypto Mining Tax

Crypto mining income is taxable as ordinary income the moment coins land in your wallet, at fair market value on that day. When you sell, capital gains tax applies on any appreciation. Business miners can deduct electricity, hardware, pool fees, and other operational costs; hobby miners cannot deduct any of it.

The classification question — hobby or business — is worth resolving early if you’re mining at any meaningful scale. The deduction difference isn’t marginal; it can represent tens of thousands of dollars in taxable income. And the record-keeping obligation starts from the first reward, not from when you decide to take things seriously.

If you’re moving serious volume, a crypto-specific CPA earns back their fee in the first year. The complexity of deduction optimization, cost basis strategies, and entity structure choices is exactly where professional guidance compounds.

Want to understand how crypto works at a deeper level? Our guide to what cryptocurrency is and how it works covers the fundamentals. And if you’re evaluating exchanges to sell mined coins, our full crypto exchange and broker reviews can help you compare your options.

Frequently Asked Questions

Is mining income taxable even if I don’t sell the coins?

Yes — and this surprises a lot of miners. The IRS taxes mining rewards as ordinary income at the moment of receipt, based on fair market value in USD on that date. Holding the coins afterward doesn’t defer the income tax obligation. It only starts the holding period clock for capital gains treatment when you eventually sell.

What’s the difference between hobby and business crypto mining for tax purposes?

Hobby miners report gross mining income on Schedule 1 and can’t deduct any expenses; the Tax Cuts and Jobs Act of 2017 eliminated those deductions. Business miners file on Schedule C, deduct electricity, hardware, pool fees, and other operational costs, but also owe self-employment tax (15.3%) on net profit. For most operations with real costs, the deductions make business classification the better financial outcome despite the SE tax.

Do I need to pay taxes on mining pool rewards?

Yes. Pool rewards are taxable in the same way as solo mining rewards — ordinary income at FMV on receipt. The pool fees paid are deductible as a business expense if you qualify as a business miner. Track what actually arrives in your wallet (net of pool deductions) to avoid over-reporting income.

What happens if I don’t report crypto mining income?

The IRS has blockchain analytics capabilities and increasingly sophisticated exchange data through Form 1099-DA requirements. Unreported mining income results in back taxes plus interest and penalties. Willful evasion carries criminal exposure. The blockchain is permanent. Transactions don’t disappear. Practically speaking, it’s a question of when the IRS finds it, not whether.

Can I deduct mining losses if the operation becomes unprofitable?

Business miners can deduct operating losses in years where expenses exceed income, subject to at-risk and hobby loss rules. Capital losses on hardware sold below purchase price are also deductible, up to $3,000 annually against ordinary income, with remaining losses carried forward to future years. Hobby miners cannot deduct losses of any kind.

Our Review Methodology

We evaluate each post based on thorough research, credibility of sources, accuracy of information, and relevance to our readers. Our editorial team follows strict guidelines to ensure all content meets high standards of quality.

Disclaimer

The content in this article is provided for informational purposes only and does not constitute financial, investment, or professional advice. Always do your own research before making any decisions.