TL;DR: A crypto liquidity pool is a smart contract holding two tokens that anyone can trade against. You deposit assets, earn a cut of every trade that passes through, and collect LP tokens as your claim check. The catch: your position can lose value against simply holding — that’s impermanent loss. Uniswap’s liquidity pools alone process $7.24 billion in weekly volume (DeFiLlama, April 2026), so there’s real money here — and real risk. Read on before you deposit.

What Is a Liquidity Pool in Crypto?

Over $86 billion is locked across DeFi protocols as of April 2026, down from a peak above $100 billion following the KelpDAO exploit. Most of that capital sits in liquidity pools — the engine that makes decentralized trading possible.

The simplest way to think about a liquidity pool: it’s a pot of two cryptocurrencies locked in a smart contract. When someone wants to swap Token A for Token B, they don’t need another person willing to sell — they trade against the pot. The pot always has tokens available. Trading never stops at 3am on a Sunday.

That’s the pitch, anyway.

Liquidity pools exist because traditional order books don’t work on blockchains the way they work on Binance. Order books need constant updates — every bid and ask is a transaction. On Ethereum, every transaction costs gas. Running a Nasdaq-style order book on-chain would cost traders a fortune in gas before a single trade cleared. So instead, DeFi uses automated market makers (AMMs) — algorithms that set prices based on pool ratios, not bids and asks. Uniswap popularized this, and now it’s the foundation of most decentralized exchanges. If you’re curious how centralized vs decentralized crypto systems compare at a higher level, that’s worth reading first.

LP Tokens: Your Receipt for Depositing

When you deposit assets into a pool, the protocol mints LP tokens and sends them to your wallet. These represent your proportional share of the pool — not a fixed number of tokens, but a percentage. If you own 2% of all LP tokens for an ETH/USDC pool, you’re entitled to 2% of both ETH and USDC in that pool, plus 2% of all accrued trading fees.

To exit, you burn your LP tokens. The protocol sends back your share of whatever is in the pool at that moment — which may be different quantities of each token than what you put in. More on that when we get to impermanent loss.

How Do Liquidity Pools Work?

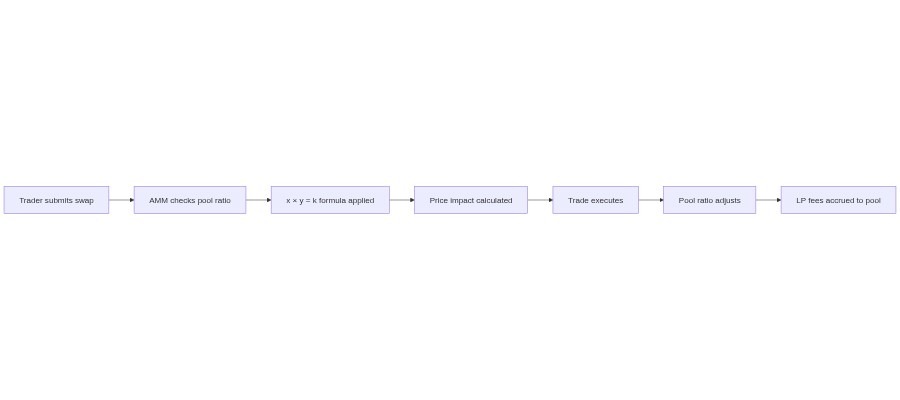

At the heart of every AMM pool is one formula: x × y = k.

Here, x is the quantity of Token A in the pool, y is the quantity of Token B, and k is a constant that never changes. When a trader buys Token A, they put Token B in. The pool’s Token A supply drops; its Token B supply rises. The product x × y stays equal to k. Prices adjust automatically.

Worked example. Say a pool starts with 100 ETH (x) and 300,000 USDC (y). k = 30,000,000. A trader wants to buy 10 ETH. They’ll pay in USDC until the formula balances: the new pool has 90 ETH, which means y must equal 30,000,000 / 90 = 333,333 USDC. The trader paid ~33,333 USDC for 10 ETH — an effective price of $3,333 per ETH. The starting price was $3,000. That gap is slippage, and it grows as trade size increases relative to pool depth.

What Happens During a Trade (and Why Arbitrage Is Everywhere)

Price impact is what keeps AMM prices tied to reality. If ETH trades at $3,000 everywhere else but your pool is now pricing it at $3,333, arbitrage traders immediately step in. They buy ETH cheaply on other exchanges, sell it into your pool at the inflated price, and pocket the spread. That rebalancing push brings pool prices back in line with market prices — usually within minutes, often seconds.

This constant rebalancing is actually the mechanism that produces impermanent loss. Arbitrageurs extract value from the pool every time prices drift. Liquidity providers are on the other side of that trade, and it costs them.

How Do You Earn Money from a Liquidity Pool?

Uniswap generated $227.4 million in trading fees in a single 30-day period as of April 2026, all distributed pro-rata to liquidity providers (CoinLaw, April 2026). Every pool passes some fraction of each trade back to the people who funded it. That’s the deal: your capital enables trading, you get paid for it.

The fee structure varies by platform and pool. Uniswap v3 has three tiers: 0.05% for stablecoin pairs, 0.30% for standard pairs, and 1% for exotic or high-volatility pairs. Curve Finance runs tighter — often 0.04% — because its stablecoin pools don’t need as much margin to attract capital.

What that translates to in annual yield depends on volume. A stablecoin pool on Curve yielding 4.2% APY on $2,000 is very different from a high-volatility meme coin pool offering 180% APY on $200. Both quotes are real. Neither is guaranteed.

Rough APY ranges as of early 2026:

- Stablecoin pairs (USDC/USDT, DAI/USDC): 2–6% — low risk, predictable

- Major pairs (ETH/USDC, WBTC/ETH): 4–15% — varies with market activity

- Long-tail/volatile pairs: 20–100%+ — high fee income, high IL exposure

Yield Farming and Liquidity Mining Rewards

Some protocols add another layer. In yield farming — or liquidity mining — the protocol distributes its own governance token on top of trading fees, as an incentive to attract capital. You stake your LP tokens in a farm, and the protocol drips tokens to you in proportion to your share.

The math breaks down like this: your total return is fees earned + token rewards – impermanent loss. Token rewards can look spectacular at launch. They almost never stay there. In 2021, some pools offered 500%+ APY in native tokens. Within months those tokens had lost 90% of their value. Fair warning: yields that look too good to be true are funded by inflation. Ask where the money comes from before you deposit.

What Is Impermanent Loss — and Should You Worry About It?

Research by Bancor and IntoTheBlock found that over 51% of Uniswap v3 liquidity providers were unprofitable — their impermanent losses exceeded the trading fees they collected (IntoTheBlock/Bancor research, 2025). A 2025 MEXC Research study put it more starkly: 54.7% of LPs in volatile token pairs lost money outright.

Impermanent loss is what happens when the price ratio of your two tokens shifts after you deposit. You deposited a 50/50 split by value; when prices change, the AMM rebalances you toward more of the cheaper token and less of the expensive one. When you withdraw, you have a different mix than you put in — often worth less than if you’d simply held both tokens in your wallet.

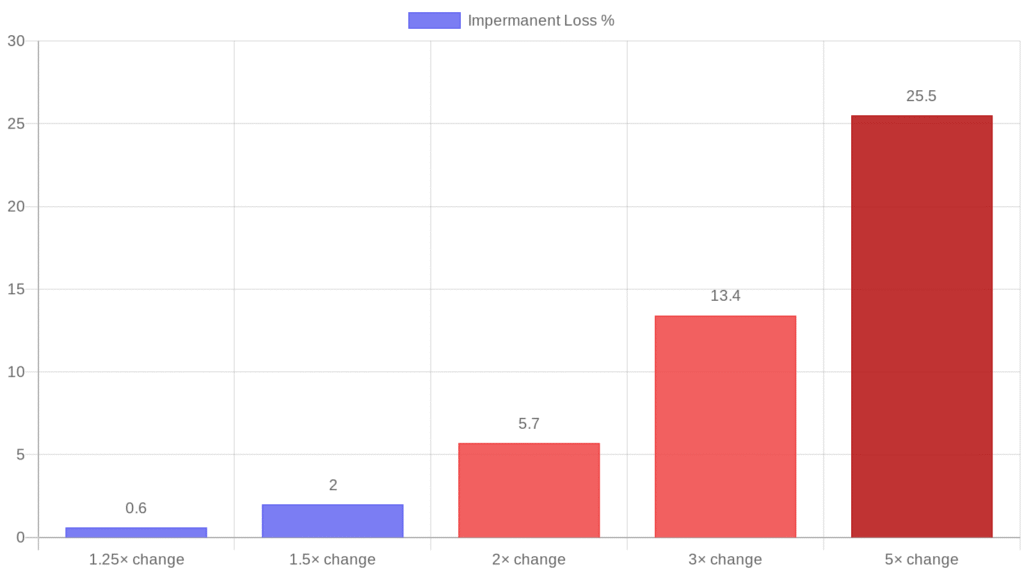

Here’s the math. At a 2× price change in one token, you lose approximately 5.7% versus holding. At a 5× change, that’s 25.5%. The word “impermanent” is technically accurate — if prices return exactly to your entry point, the loss reverses. In practice, prices rarely trace back exactly. When you withdraw at a different ratio, that loss crystallizes.

I ran a small ETH/USDC position on Uniswap last year — deposited at $2,800 ETH, watched ETH climb to $4,200, and pulled out when it dropped back to $3,400. On paper I made money versus cash. Against simply holding ETH, I underperformed by about 8%. The fees helped. They didn’t fully close the gap. That’s the trade-off.

When Fees Beat Impermanent Loss

Impermanent loss isn’t automatic ruin. High-volume pools generate enough fees to offset it. The USDC/USDT pool on Curve earns tiny fees per trade — but it processes billions in daily volume, and the stablecoin pairing means price ratios barely shift. Impermanent loss is near-zero. Fees compound steadily.

The danger zone is volatile pairs with low volume. You get the full IL exposure without enough fee income to compensate. SUSHI-WETH learned this the hard way in September 2020 — SUSHI dropped over 80%, and LPs faced losses exceeding 50% of their deposited value. The fees weren’t close to covering it.

The honest calculation: before entering any pool, divide the estimated annual fee yield by the expected price volatility range. If a 2× move seems plausible for one of your tokens (and it usually is in crypto), you need roughly 5.7%+ in annual fee income just to break even versus holding. Stablecoin pools clear that bar easily. Exotic altcoin pools rarely do.

How Does a Uniswap Liquidity Pool Work?

Uniswap processed $7.24 billion in weekly trading volume as of April 10, 2026, across 36 chains (DeFiLlama, April 2026). It’s the largest DEX by volume and the protocol most people encounter first when they look into liquidity provision.

Uniswap uses the x × y = k formula described above. In v2, the liquidity you deposit is spread uniformly across the entire price range — from $0 to infinity for a given pair. That sounds thorough. In practice, it means your capital sits idle at price ranges that trading never touches.

Concentrated Liquidity: What Uniswap v3 Changed

Uniswap v3 introduced concentrated liquidity in 2021. Instead of spreading your capital across the full curve, you specify a price range — say, ETH between $2,500 and $4,000. Your capital only earns fees when ETH trades within that range. When price exits your range, you stop earning entirely.

This is more capital-efficient. Within the active range, you might generate 10-50× the fees of a v2 position the same size. The downside: if price moves outside your range and you don’t rebalance, your position converts entirely into the underperforming token. Concentrated liquidity doesn’t reduce impermanent loss — it concentrates it too.

For most people entering DeFi for the first time, v2-style uniform distribution is simpler and more forgiving. For experienced LPs who actively monitor positions, v3’s concentrated pools can generate substantially better returns.

Uniswap Fee Tiers

| Pool Type | Fee Tier | Best For |

|---|---|---|

| Stablecoin pairs (USDC/USDT) | 0.05% | Tight spreads, high volume |

| Standard pairs (ETH/USDC) | 0.30% | Most common pairs |

| Exotic/volatile pairs | 1.00% | High-volatility, low-liquidity tokens |

Choosing the wrong fee tier is a common mistake. If most LPs in a pair have chosen 0.30% but you deploy at 1.00%, volume routes around you — you capture no fees and hold the IL risk anyway.

What Are the Biggest Risks of Liquidity Pools?

Impermanent loss gets the most press. It’s not always the biggest risk. Smart contract exploits have wiped out hundreds of millions in locked liquidity across DeFi’s short history.

Smart contract vulnerabilities are the existential concern. Liquidity pools are code. Code has bugs. The Harvest Finance exploit in 2020 drained $33.8 million through a flash loan attack on its liquidity pool contracts (Hacken, 2026). Audits reduce risk — they don’t eliminate it. Unaudited protocols, or protocols that quietly upgrade their contracts without community review, carry materially higher risk.

Rug pulls are the more deliberate version of the same problem. A team deploys a pool, attracts liquidity with high rewards, then drains the pool’s smart contract of all assets. AnubisDAO lost $60 million this way in 2021 — in a single transaction, the liquidity vanished. Not all rug pulls are this clean. Some are gradual — rewards reduced, team disappears, token price drifts to zero.

Slippage in shallow pools is the mundane version. A pool with $50,000 in liquidity can’t execute a $10,000 trade cleanly — price impact will be brutal. This matters most when you’re exiting a position in a token that’s falling fast. You can’t always get out at the price you see.

Before depositing: check whether the protocol has been audited (and who by), confirm the contract can’t be upgraded without timelock or governance approval, and look at pool depth relative to your position size. If you need a wallet to get started, the MetaMask wallet review covers what you need for DeFi access.

How to Join a Liquidity Pool (Step by Step)

The mechanical process is straightforward. The hard decisions — which pair, which fee tier, how much — come before you open the app.

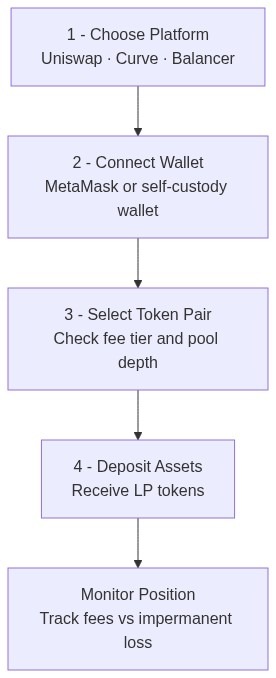

Step 1 — Choose your platform. Uniswap for Ethereum-native pairs. Curve if you’re using stablecoins or correlated assets. PancakeSwap if you’re on BNB Chain. Each has its liquidity concentrations and its quirks. Not all platforms have equal security track records.

Step 2 — Connect your wallet. You’ll need a self-custody wallet — MetaMask is the most common for Ethereum-based DEXs. Make sure your wallet holds both tokens in the pair you’re joining, plus ETH (or the chain’s native token) for gas.

Step 3 — Select the token pair and fee tier. On Uniswap v3, you’ll also need to set your price range for concentrated liquidity. If that’s too complex for a first attempt, some aggregators offer auto-managed positions.

Step 4 — Deposit and confirm. Review the transaction details — specifically the minimum amounts you’ll receive if price moves before the transaction confirms. That’s the slippage tolerance setting. Hit confirm, pay gas, and your LP tokens arrive.

Worth knowing before you deposit: you can check a pool’s trading volume, TVL, and historical fee APY on DeFiLlama or the protocol’s own analytics page before committing capital. Treat the APY figure as a trailing indicator of past activity, not a promise of future returns.

The Bottom Line on Crypto Liquidity Pools

Liquidity pools let you put idle crypto assets to work — earning a share of trading fees from a protocol processing billions in volume each week. Uniswap alone generated $227.4 million in fees over 30 days (CoinLaw, April 2026), all distributed to people who funded the pools. That’s real income, and it flows to anyone willing to participate.

The cost is impermanent loss and smart contract risk. For stablecoin pairs, impermanent loss is minimal and fees compound predictably. For volatile pairs, IL can eat your returns entirely — and over 51% of Uniswap v3 volatile-pair LPs found out the hard way.

The honest answer to “is it worth it?” is: it depends on the pair. Stablecoin pools are an efficient place to put idle USDC or USDT. Volatile altcoin pools are speculation disguised as income generation. Know which one you’re actually doing before you deposit.

For more context on how cryptocurrency works at a foundational level, or to explore our full library of crypto trading guides, both are worth your time before committing capital to DeFi.

Frequently Asked Questions

What is a crypto liquidity pool?

A crypto liquidity pool is a smart contract holding two tokens that traders swap against directly, without a counterparty. Deposits are made by liquidity providers, who earn a portion of every trading fee in return. Most pools use the constant product formula (x × y = k) to set prices automatically. The total value locked across DeFi liquidity pools exceeded $86 billion as of April 2026.

Is impermanent loss permanent?

Only when you withdraw. While your assets stay in the pool, the loss is unrealized — if token prices return exactly to your entry ratio, it reverses completely. In practice, prices rarely trace back precisely. Withdrawing at a different price ratio than you entered locks in whatever loss has accumulated to that point. High fee income from busy pools can offset it; volatile pairs with low volume often can’t.

How much can you earn from a liquidity pool?

It depends heavily on the pair and platform. Stablecoin pools on Curve typically yield 2–6% APY with minimal IL. Major pairs like ETH/USDC on Uniswap can generate 4–15% in active markets. High-volatility pairs may show 50–100%+ yields, but those figures come with proportionally higher impermanent loss risk. Treat any APY quote as a trailing indicator, not a forward guarantee — rates change as volume and pool depth shift.

What’s the difference between staking and a liquidity pool?

Staking involves locking a single token — usually to support a network’s consensus mechanism — and earning staking rewards. Liquidity provision means depositing two tokens into a trading pair and earning fees from swaps. Staking carries no impermanent loss risk. Liquidity pools do. Staking rewards are typically more predictable; liquidity pool returns depend on trading volume.

What is the safest type of liquidity pool?

Stablecoin pools between correlated or pegged assets — like USDC/USDT or DAI/USDC on Curve — carry the lowest impermanent loss risk, since both tokens are designed to hold the same value. Risk then shifts primarily to smart contract vulnerability and the stability of the stablecoins themselves. Pools on long-established, heavily audited protocols (Uniswap, Curve, Aave) are generally safer than newer or unaudited alternatives, though no DeFi pool is risk-free.

Our Review Methodology

We evaluate each post based on thorough research, credibility of sources, accuracy of information, and relevance to our readers. Our editorial team follows strict guidelines to ensure all content meets high standards of quality.

Disclaimer

The content in this article is provided for informational purposes only and does not constitute financial, investment, or professional advice. Always do your own research before making any decisions.