You sold some ETH last year. Made a decent profit. Now tax season arrives and you’re wondering whether the IRS is actually paying attention to that. They are. And unlike your stock broker, no one automatically withheld anything.

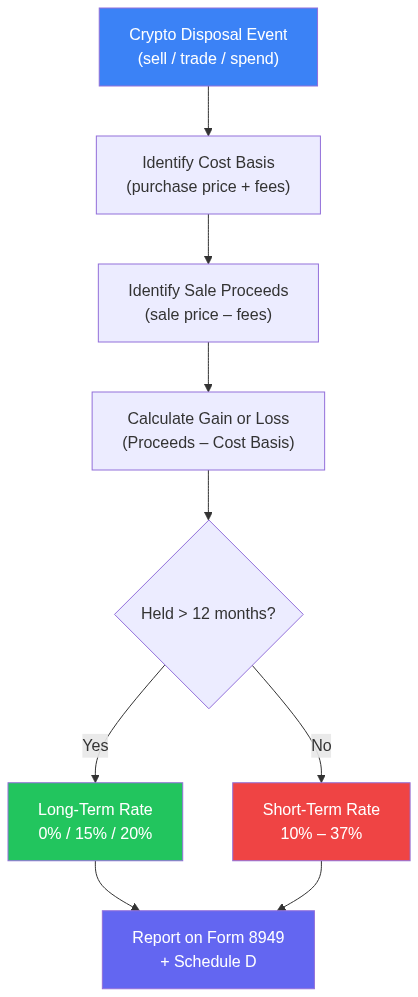

Crypto capital gains tax works like this: the IRS treats cryptocurrency as property, not currency. Every time you sell, trade, or spend crypto at a profit, that’s a taxable event. The rate you pay depends almost entirely on one thing — how long you held it.

Here’s what’s changed for 2026: centralized exchanges operating in the US are now required to report your capital gains and losses directly to the IRS via Form 1099-DA. So if you were betting on crypto staying off the radar, that window closed.

This guide covers the 2025 and 2026 tax rates, how to calculate what you actually owe, and a few legal ways to reduce the bill.

What Triggers Crypto Capital Gains Tax?

Not every crypto transaction generates a taxable event. Buying Bitcoin and leaving it in your wallet isn’t taxable. The tax kicks in when you dispose of the asset.

Disposals the IRS counts:

- Selling crypto for USD or any fiat currency

- Trading one crypto for another — swapping ETH for SOL counts as a disposal of your ETH

- Spending crypto on goods or services — yes, buying a coffee with Bitcoin is technically a taxable event

- Earning crypto income — staking rewards, mining, airdrops, and payment for work are taxed as ordinary income at the moment you receive them (not when you sell)

What’s not taxable: buying crypto, transferring between wallets you own, and gifting crypto below the annual exclusion threshold ($18,000 per person in 2025).

That distinction between capital gains and ordinary income matters more than most new crypto holders realize. Staking rewards aren’t capital gains — they’re income, taxed the day you receive them. When you eventually sell those staking rewards, then you also owe capital gains on any appreciation since you received them. Two separate tax events from one holding.

Short-Term vs. Long-Term Capital Gains Crypto: The Rate Gap Is Huge

The single most important factor in your crypto tax rate isn’t your income. It’s your holding period.

Hold for 12 months or less — short-term gains, taxed as ordinary income. Hold for more than 12 months — long-term gains, which get preferential rates.

Short-term capital gains tax rate on crypto (2025, taxed as ordinary income):

| Taxable Income (Single Filer) | Rate |

|---|---|

| $0 – $11,925 | 10% |

| $11,926 – $48,475 | 12% |

| $48,476 – $103,350 | 22% |

| $103,351 – $197,300 | 24% |

| $197,301 – $250,525 | 32% |

| $250,526 – $626,350 | 35% |

| Over $626,350 | 37% |

Long-term capital gains tax rate on crypto (2025, single filer):

| Taxable Income (Single Filer) | Rate |

|---|---|

| $0 – $48,350 | 0% |

| $48,351 – $533,400 | 15% |

| Over $533,400 | 20% |

Source: IRS Publication 550 (2024), updated for 2025 tax year.

The difference between these schedules is the entire argument for holding. Someone earning $80,000 in taxable income pays 22% on a short-term crypto gain but 15% on the same amount held long-term. On a $50,000 profit, that’s $3,500 saved just by waiting past the 12-month mark.

At the top bracket, it’s starker: 37% short-term versus 20% long-term. That’s not a minor adjustment — it’s the difference between keeping 63 cents on the dollar and keeping 80 cents.

How Do You Calculate Crypto Capital Gains?

The formula is simple. The execution is not.

Capital gain = Sale proceeds − Cost basis

Cost basis is what you paid for the crypto, including any transaction fees. Proceeds are what you received when you sold.

Worked example: You bought 1 ETH for $2,200 (including $5 gas fee). Eight months later you sold it for $3,100 (after $8 in fees). Your proceeds are $3,092, your cost basis is $2,205, your gain is $887. Held for eight months, so it’s short-term — taxed at your income rate, say 22%. Tax owed: ~$195.

Same scenario but you waited 14 months. Now it’s long-term. At $80K taxable income, your long-term rate is 15%. Tax owed: ~$133. Same trade, same profit — different holding period saves $62.

Why it gets complicated:

Most people don’t hold one token bought once. They buy in tranches, trade between coins, earn staking rewards, and move across five exchanges. Each purchase has a different cost basis. Each trade is a separate taxable event.

The IRS allows several cost basis methods — FIFO (first in, first out), HIFO (highest in, first out), and specific identification. HIFO typically produces the lowest taxable gain because you’re matching your sale against your highest-cost purchase. Specific identification is even more precise but requires meticulous records.

Fair warning: as of 2025, many tax software platforms still default to FIFO unless you explicitly choose otherwise. Check your settings before you let it run.

What Is Crypto CGT — and Does It Apply Outside the US?

“CGT” — capital gains tax — is the term used in the UK and Australia, where tax treatment of crypto follows the same general logic but with different thresholds and rules.

United Kingdom. HMRC classifies crypto as property. Disposals trigger CGT. For the 2025/26 tax year, UK taxpayers get a £3,000 annual CGT exemption. Above that: basic rate taxpayers pay 18%, higher rate taxpayers (income over £50,270) pay 24%. Crypto held over one year gets no preferential long-term rate in the UK — the holding period doesn’t change your rate the way it does in the US. Staking and mining income is taxed as miscellaneous income.

Australia. The ATO treats crypto as an asset for CGT purposes. Gains are included in assessable income and taxed at your marginal rate (0–45%). The notable carve-out: hold for more than 12 months and you get a 50% CGT discount on the gain. On a $10,000 gain, you’re only assessed on $5,000. For someone in the 34.5% bracket, that cuts the real tax rate to 17.25%.

The bottom line for non-US traders: the 12-month holding threshold shows up in both the US and Australia as a meaningful line. In the UK it doesn’t change your rate, but the £3,000 annual exemption is worth timing around.

Do You Owe the Net Investment Income Tax (NIIT)?

Possibly, and it catches a lot of crypto holders off guard.

If your modified adjusted gross income (MAGI) exceeds $200,000 (single) or $250,000 (married filing jointly), you owe an additional 3.8% on your net investment income — including crypto capital gains. This is on top of your regular capital gains rate.

At the 20% long-term rate, NIIT pushes your effective federal rate to 23.8%. Add your state’s capital gains tax on top — California hits 13.3% — and high earners in high-tax states can face an all-in rate above 37% even on long-term gains.

How to Reduce Your Crypto Capital Gains Tax Bill (Legally)

There aren’t many legal ways to reduce a crypto tax bill, but the ones that exist are actually useful.

Tax-loss harvesting. Crypto has no wash-sale rule. Stocks have one — you can’t sell a stock at a loss and buy it back within 30 days while still claiming the loss. Crypto doesn’t have that restriction (though proposed legislation has periodically tried to add one, so this could change). This means you can sell a losing position, book the loss to offset gains elsewhere, and immediately rebuy. Dollar-cost average out and back in on the same day if you want.

Losses offset gains dollar-for-dollar. If you have $20,000 in gains and $15,000 in losses, you’re only taxed on $5,000 net. If losses exceed gains, you can deduct up to $3,000 against ordinary income per year and carry the rest forward.

Hold past 12 months. Obvious, but the math is compelling — see the worked examples above. The 22% vs 15% gap isn’t trivial.

Maximize retirement account contributions. If your employer’s 401(k) offers a crypto option (Fidelity Crypto launched in 2022), gains inside a traditional 401(k) are tax-deferred. In a Roth 401(k) or Roth IRA, gains are tax-free if the account meets qualifying rules. Bitcoin ETFs are available in IRAs now — this is a legitimate strategy.

Gift appreciated crypto strategically. Gifting crypto to someone in the 0% long-term gains bracket (income under $48,350 for singles in 2025) means they pay zero federal tax when they sell, as long as the gain qualifies as long-term. If you’ve got family members with lower income, this is worth looking at with a tax advisor.

Staking, Mining, and DeFi: How These Are Actually Taxed

These income streams trip people up because they look like gains but are treated differently.

Staking rewards are ordinary income, taxed at your income rate on the day you receive them. The value at receipt is your cost basis. When you eventually sell the tokens, any gain (or loss) above that cost basis is a capital gain.

Mining income follows the same logic. The fair market value of mined coins on the day you receive them is ordinary income. Deductible mining expenses (electricity, equipment depreciation) reduce this, but mining at scale creates self-employment tax exposure too.

Airdrops received for doing nothing — just holding an eligible token — are ordinary income at fair market value on receipt. Airdrops received in exchange for completing tasks may be treated as compensation, taxed the same way.

DeFi is messier. Providing liquidity to a pool involves depositing tokens and receiving LP tokens in return. The IRS hasn’t issued clear guidance on whether depositing tokens into a liquidity pool is a taxable disposal. Many tax professionals treat it as a taxable exchange. Removing liquidity and receiving different token amounts than you deposited (due to impermanent loss) complicates the cost basis further.

If you’re running serious DeFi volume — multiple protocols, frequent liquidity moves, yield farming across chains — a crypto-specialized CPA is worth the fee. The reporting complexity is real, and the penalties for misreporting aren’t minor.

What Changes with Form 1099-DA in 2026?

Starting January 1, 2026, all centralized cryptocurrency exchanges operating in the United States must report customer capital gains and losses directly to the IRS via Form 1099-DA. This is a significant change.

Previously, exchanges might send you a 1099-B or a summary report. As of 2026, the IRS gets a copy too — automatically. Under-reporting becomes harder to accidentally do and easier for the IRS to catch.

What’s being reported:

- Your proceeds from crypto sales

- Your cost basis (for purchases made on or after January 1, 2026)

- Whether the gain is short-term or long-term

The cost basis reporting on the 1099-DA only covers purchases made on the exchange on/after January 1, 2026. Crypto bought before that date — or on different platforms — still requires you to track and report cost basis yourself. Most tax software imports transaction data from exchanges via API to handle this.

Decentralized exchanges (DEXs) and self-custody wallets aren’t covered by the 1099-DA rule. That responsibility stays with you.

Alina’s Take

The biggest mistake I see crypto holders make isn’t fraud — it’s chaos. No records, seven exchanges, staking rewards they forgot about, LP positions they treated as parking. The tax obligation was real the entire time; they just didn’t know it existed until they got a notice.

If your crypto activity is simple — bought some BTC and ETH on one exchange, haven’t traded much — a standard tax software handles it fine. Koinly, CoinLedger, and TokenTax all import transaction history via API and generate the forms you need.

If you’ve got multiple chains, DeFi positions, bridging transactions, or staking at scale: find a crypto-specialized CPA before you file, not after. The IRS has significantly ramped up enforcement capability. Blockchain analytics firms including Chainalysis have contracts with the IRS that let them trace transactions across chains. The “it’s anonymous” assumption stopped being realistic years ago.

One more thing. The wash-sale rule gap — the ability to harvest losses and immediately rebuy — is genuinely useful while it lasts. There’s been bipartisan legislation proposed to close it. Take advantage while it’s still legal, and don’t bet on it staying available forever.

Frequently Asked Questions

How much tax do you pay on crypto gains?

It depends on how long you held and your total taxable income. Short-term gains (held 12 months or less) are taxed at ordinary income rates: 10%–37% depending on your income bracket. Long-term gains (held more than 12 months) are taxed at 0%, 15%, or 20%. For most people earning between $48,000 and $533,000, the long-term rate is 15%.

Is crypto capital gains tax the same as regular capital gains tax?

Yes. The IRS treats crypto as property, so the same capital gains rules apply as for stocks, real estate, or other assets. Short-term and long-term brackets are identical. The main difference from stocks: crypto has no wash-sale rule, so you can harvest losses and immediately rebuy.

Do you pay taxes on crypto if you don’t sell?

No. Holding crypto isn’t a taxable event. Tax is triggered when you sell, trade, spend, or earn crypto — not by simply owning it, regardless of how much its value changes.

What is the crypto CGT discount in Australia?

Australian crypto holders who keep an asset for more than 12 months are entitled to a 50% capital gains tax (CGT) discount. This means only 50% of the capital gain is included in your assessable income and taxed at your marginal rate. This discount doesn’t apply to short-term holds or to crypto held as business stock.

What’s the crypto tax rate in the UK?

In the UK, crypto capital gains are taxed at 18% for basic rate taxpayers and 24% for higher rate taxpayers, after a £3,000 annual exemption. Unlike the US, the UK doesn’t reduce rates for long-term holds — the holding period doesn’t affect your CGT rate. Income from crypto (staking, mining) is taxed as miscellaneous income at your income tax rate.

What is Form 1099-DA?

Form 1099-DA is a new IRS reporting form effective January 1, 2026. US centralized crypto exchanges must file it for customers, reporting proceeds from crypto sales and (for purchases on/after Jan 1, 2026) cost basis. The IRS receives a copy. It’s similar to the 1099-B used for stock brokerage accounts.

This article is for educational purposes only and does not constitute financial or tax advice. Tax rules vary by jurisdiction and change frequently — speak to a qualified tax professional before making decisions based on this information.

Our Review Methodology

We evaluate each post based on thorough research, credibility of sources, accuracy of information, and relevance to our readers. Our editorial team follows strict guidelines to ensure all content meets high standards of quality.

Disclaimer

The content in this article is provided for informational purposes only and does not constitute financial, investment, or professional advice. Always do your own research before making any decisions.