You sold some ETH in October. Collected staking rewards all year. Maybe swapped a few tokens on a DEX at 2am. Now April is here, and you’re staring at a spreadsheet that makes zero sense.

Good news: crypto taxes aren’t as unknowable as they seem. Bad news: they’re not simple either — and the IRS is paying a lot more attention than it used to. More than 55 million U.S. adults now hold digital assets, and exchanges are issuing tens of millions of new reporting forms. The system is tightening.

This guide covers what you actually need to know: which forms to use, what counts as a taxable event, how to calculate your gains, and what deadlines to hit.

The IRS treats crypto as property. You report capital gains on Form 8949 + Schedule D, and income (staking, mining, airdrops) on Schedule 1 or Schedule C. New for 2025: Form 1099-DA from your exchange. Tax deadline is April 15, 2026. Miss it without an extension and penalties start immediately. Crypto tax software — Koinly, CoinLedger, or TaxBit — can handle the heavy lifting if your transaction history is complicated.

How the IRS Treats Cryptocurrency

The IRS ruled on this in 2014. IRS Notice 2014-21 was blunt: cryptocurrency is property, not currency. That single classification shapes everything about how you report it.

What it means in practice: every time you dispose of crypto — sell it, trade it, spend it — you’ve got a tax event. Just like selling stock. You calculate the difference between what you paid (cost basis) and what you received (sale price), and that difference is either a capital gain or a capital loss.

Holding crypto doesn’t trigger a tax event. Buying it doesn’t either. The trigger is disposal.

The IRS has added a digital asset disclosure question directly on Form 1040 since 2019, and it’s gotten more prominent every year. For 2025, the question asks: “At any time during 2025, did you receive, sell, exchange, or otherwise dispose of any digital asset?” You must answer it. Checking “No” when the answer is “Yes” is not a good idea.

What Counts as a Taxable Crypto Event?

Short version: disposal triggers taxes. Income triggers taxes. Just having crypto in a wallet doesn’t.

Taxable events include:

- Selling crypto for fiat — exchanging BTC for dollars triggers capital gains or losses

- Crypto-to-crypto trades — swapping ETH for SOL is a disposal of ETH. The IRS sees it the same as selling ETH for dollars, then buying SOL. Each swap is a separate taxable event.

- Spending crypto — paying for goods or services with crypto realizes a gain or loss equal to the difference between cost basis and fair market value at the time of payment

- Staking and mining rewards — these are ordinary income, taxed at your normal income rate when you receive them. The IRS treats them as income at fair market value on the day you receive them.

- Airdrops — generally taxed as ordinary income when received, at fair market value

- DeFi activity — lending interest, liquidity pool rewards, and yield farming proceeds are all ordinary income

Not taxable:

- Buying crypto with fiat — you’ve just acquired property

- Transferring between your own wallets — you’re moving property, not disposing of it

- Holding without selling

- Gifting crypto (up to $19,000 per recipient in 2025 without gift tax implications)

- Donating to a qualified charity

Here’s the one that trips people up most: crypto-to-crypto swaps. Every DEX trade, every time you swap one token for another, is a taxable disposal. I’ve seen people rack up hundreds of taxable events in a single yield-farming session without realizing it. Those small swaps add up — and the IRS now has Form 1099-DA paperwork from exchanges to match against your return.

Which IRS Forms Do You Need for Crypto?

You probably need more than one. Here’s what each does.

Form 1040 — your main tax return. Includes the digital asset question (see above). Everyone filing a federal return needs this.

Form 8949 — this is where the work happens. You list every single capital gain and loss transaction here: date acquired, date sold, proceeds, cost basis, and gain/loss. One row per transaction. If you made 500 trades, that’s 500 rows — or you can summarize by exchange if you attach a complete statement.

Schedule D — summarizes your Form 8949 totals. Short-term gains, long-term gains, net result. Feeds into your 1040.

Form 1099-DA — new for the 2025 tax year. Centralized exchanges (Coinbase, Kraken, Gemini, and others) now issue this form showing gross proceeds from digital asset sales. You’ll receive it by mid-March 2026. Fair warning: the 1099-DA shows proceeds but not cost basis in most cases — so you still need your own records to calculate actual gains.

Form 1099-MISC — some platforms use this to report staking rewards, referral bonuses, and other non-trading crypto income over $600. If you earned more than $600 in staking rewards from a custodial platform, check whether they issued a 1099-MISC.

Schedule 1 or Schedule C — staking rewards and mining income you report here. Schedule 1 for casual activity; Schedule C if you’re running a mining operation as a business.

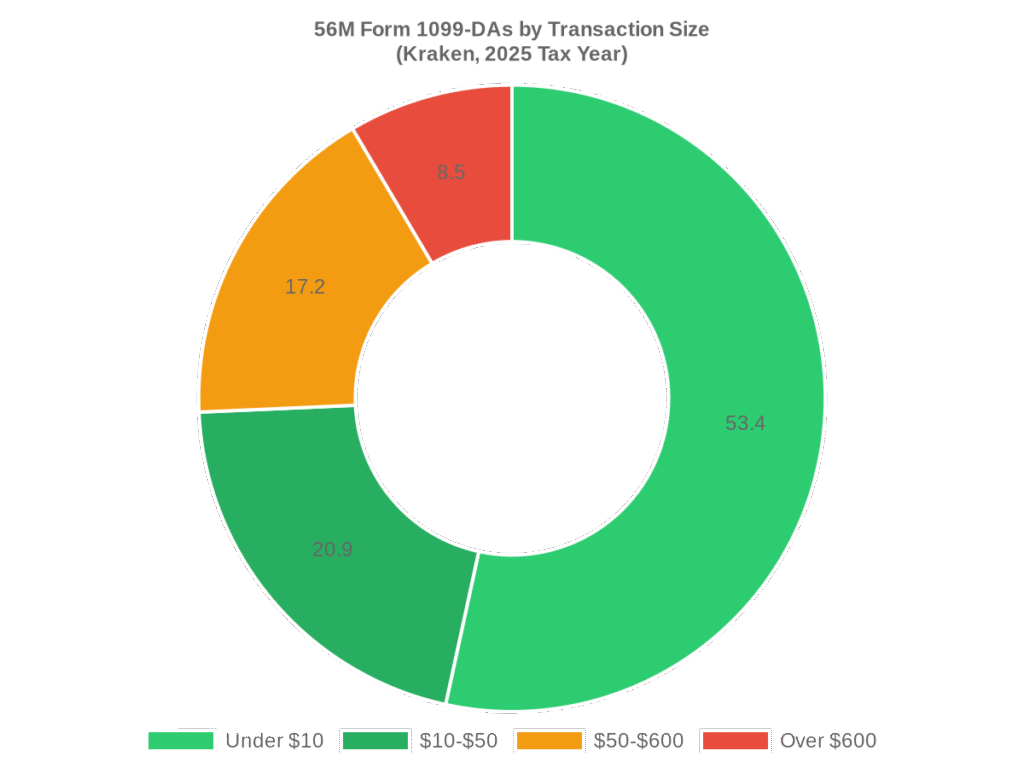

The scale of this is worth noting. Kraken alone issued 56 million Form 1099-DAs for the 2025 tax year (Kraken blog, 2026) — and 74.3% of those covered transactions under $50. The IRS is getting paperwork on small transactions that most traders never thought twice about.

How to Calculate Your Crypto Capital Gains

The formula is simple. The execution is not.

Capital Gain (or Loss) = Sale Price − Cost Basis

Sale price is straightforward: the USD value you received, whether that’s actual dollars or the fair market value of what you got in a crypto-to-crypto swap.

Cost basis is harder. It’s what you originally paid, including any fees at purchase. If you bought 0.5 ETH for $1,200 on Coinbase, your cost basis is $1,200 (plus fees).

A worked example:

- You bought 1 ETH for $2,400 in March 2024

- You sold that ETH for $3,100 in November 2025

- Capital gain: $3,100 − $2,400 = $700

- Held more than 1 year → qualifies for long-term capital gains rates

Now flip it:

- You bought 1 ETH for $3,500 in January 2025

- You sold for $2,800 in August 2025

- Capital loss: $2,800 − $3,500 = −$700

- Held less than 1 year → short-term loss you can use to offset gains

Losses aren’t just bad news. They reduce your taxable gains dollar for dollar. If you have more losses than gains in a year, you can deduct up to $3,000 against ordinary income, and carry the rest forward to future years.

Short-Term vs. Long-Term Crypto Tax Rates

This is the clearest reason to think about hold time before you sell.

Short-term gains (held 1 year or less): taxed at your ordinary income rate — 10%, 12%, 22%, 24%, 32%, 35%, or 37% depending on your total income.

Long-term gains (held more than 1 year): taxed at preferential rates.

| Filing Status | 0% Rate | 15% Rate | 20% Rate |

|---|---|---|---|

| Single | Up to $48,350 | $48,351–$533,400 | Over $533,400 |

| Married Filing Jointly | Up to $96,700 | $96,701–$600,050 | Over $600,050 |

Source: IRS 2025 capital gains rates

The math here is real. If you’re in the 22% income bracket and you sell crypto you’ve held for 11 months, you pay 22% on that gain. Hold it one more month and you might pay 0% or 15%. That’s not a minor difference.

I’ve watched people sell ETH in November and owe a serious tax bill when they would have owed almost nothing with a 30-day wait. Sometimes market timing is the wrong frame — tax timing matters too.

What Cost Basis Method Should You Use?

The IRS allows four approaches. Which one you choose affects how much tax you owe.

FIFO (First In, First Out) — your oldest crypto is treated as sold first. This is the IRS default if you don’t specify otherwise. In a rising market, FIFO tends to produce larger taxable gains because your oldest holdings have the lowest cost basis.

HIFO (Highest In, First Out) — the lot with the highest purchase price is sold first. This generally minimizes taxable gains and is the most popular choice for active traders.

LIFO (Last In, First Out) — most recently purchased crypto is sold first. Useful in some scenarios but less common.

Specific Identification (Spec ID) — you designate exactly which units you’re selling. Most precise, but requires meticulous records and pre-sale documentation.

Here’s the catch: starting in 2025, the IRS requires wallet-by-wallet basis tracking. You can no longer pool all your holdings universally across wallets and exchanges. If you moved BTC from Coinbase to a cold wallet, you need to trace that specific lot — the universal basis approach is gone. Most crypto tax software handles this automatically, which is why it’s worth using.

How to File Crypto Taxes: Step by Step

B[Calculate Cost Basis per Wallet]; B–>C[Identify Taxable Events]; C–>D[Calculate Gains & Losses]; D–>E[Complete Form 8949]; E–>F[Summarize on Schedule D]; F–>G[Report Income on Schedule 1 or C]; G–>H[File with Form 1040 by April 15]] –> Step 1 — Gather your transaction history. Export records from every exchange, wallet, and DeFi protocol you used during 2025. Most exchanges offer a CSV export. Don’t forget accounts you stopped using mid-year — every transaction counts.

Step 2 — Collect your 1099-DA forms. Custodial exchanges should have sent these by March 13, 2026. Match them against your own records. Where there are discrepancies (and there will be), your records take precedence — the 1099-DA may not have complete cost basis information.

Step 3 — Calculate cost basis per wallet. Apply your chosen cost basis method (HIFO, FIFO, or Spec ID) to each wallet separately, not across all wallets combined.

Step 4 — Identify every taxable event. Each sale, trade, and disposal from Step 3 generates a gain or loss figure.

Step 5 — Complete Form 8949. Fill out Part I for short-term transactions (held ≤1 year) and Part II for long-term (held >1 year). List each transaction or use the summary method if you attach a complete statement.

Step 6 — Complete Schedule D. Sum your Part I and Part II totals from Form 8949. Note your net capital gain or loss.

Step 7 — Report crypto income separately. Staking rewards, mining income, and airdrops go on Schedule 1 (line 8z, “Other Income”) or Schedule C if running a crypto business. These are taxed as ordinary income.

Step 8 — File by April 15, 2026. Need more time? File Form 4868 by April 15 for an automatic six-month extension to October 15. The extension covers filing, not payment — if you owe tax, you still need to pay an estimate by April 15.

How to Lower Your Crypto Tax Bill Legally

A few strategies actually work.

Hold longer than one year. The long-term capital gains rate is almost always lower than short-term. If you’re close to the one-year mark on a position, the math often favors waiting.

Tax-loss harvesting. Selling positions at a loss to offset gains elsewhere. Unlike stocks, crypto doesn’t have a wash-sale rule — yet. You can sell BTC at a loss, realize the deduction, and buy it back the next day. The IRS has proposed wash-sale rules for crypto but they hadn’t passed as of April 2026, so this window remains open.

Donate crypto directly. If you’re giving to a qualified charity, donating appreciated crypto instead of selling it first avoids capital gains entirely. You deduct the full fair market value. For donations above $5,000, you’ll need a qualified appraisal.

Crypto IRA. Some platforms allow you to hold crypto inside a self-directed IRA. Gains grow tax-deferred (traditional IRA) or tax-free (Roth IRA). The contribution limits and rules are the same as standard IRAs. This is a longer-term play, not a quick fix.

Harvest losses before December 31. Tax-loss harvesting only works within the same tax year. Selling a losing position on January 2 does nothing for last year’s return.

Crypto Tax Software Worth Considering

If you’ve made more than a handful of transactions, doing this manually is genuinely painful. The software exists because the problem is real.

Koinly — connects to 700+ exchanges and wallets. Solid DeFi support. Pricing starts around $49 for basic tier, ~$179 for active traders with many transactions. Generates Form 8949 directly.

CoinLedger — strong exchange integrations, clean interface. Pricing similar to Koinly. Favored by users with complex DeFi histories. 500,000+ users as of 2026.

TaxBit — originally enterprise-focused, now has a consumer product. Better for institutional-scale transaction volumes. Free tier available for limited transactions.

Worth knowing before you pay: your exchange may offer free or discounted tax reports through partnerships with these tools. Coinbase, for example, has had ongoing integrations. Check your exchange’s tax center first.

None of these replace a CPA if you have a genuinely complex situation — multiple years of unreported activity, mining operations at scale, or large gains that need optimization. They’re tools, not tax advice.

What Happens If You Don’t Report Crypto?

The risk has increased significantly. Exchanges are issuing 1099-DA forms. The IRS gets a copy of every one. That means the agency can now match reported proceeds against your filed return — the same way it does with stock sales.

What you’re looking at for unreported crypto:

- Failure-to-pay penalties: 0.5% of unpaid taxes per month, up to 25%

- Failure-to-file penalties: 5% of unpaid taxes per month, up to 25%

- Accuracy-related penalties: 20% of the underpayment for negligence or substantial understatement

- Criminal penalties in egregious cases: fines up to $250,000 and up to 5 years imprisonment

If you’ve missed prior years, the IRS has a voluntary disclosure program. Filing amended returns proactively — before you receive a notice — typically results in reduced penalties. Waiting for the IRS to find you first is the expensive option.

The Bottom Line on Crypto Tax Reporting

Reporting crypto taxes comes down to tracking disposals accurately, using the right forms (8949 and Schedule D for capital gains; Schedule 1 for income), and meeting the April 15, 2026 deadline. The new Form 1099-DA has made broker reporting more formal — which means less room to miss transactions. If your transaction history is complicated, dedicated tax software handles the heavy lifting better than a spreadsheet.

For more on the exchanges you’re trading on and how they handle reporting, check out Tradelize’s exchange guides.

Frequently Asked Questions

Do I have to report crypto if I didn’t sell anything?

If you only bought and held crypto without selling, trading, spending, or earning rewards, you don’t have a reportable transaction. You still need to answer the digital asset question on Form 1040 — but if no disposal occurred, you check “No.” Holding is not a taxable event.

What is Form 1099-DA and do I need it?

Form 1099-DA is a new form for the 2025 tax year. Centralized exchanges issue it to report gross proceeds from your digital asset disposals. You’ll receive it from any regulated exchange you used in 2025 — expect it by mid-March 2026. It reports proceeds but often not cost basis, so you still need your own records to calculate actual gains.

Can the IRS track my crypto wallet?

Yes, to a meaningful extent. The IRS uses blockchain analytics firms (Chainalysis, TRM Labs, and others) to trace on-chain activity. Exchanges under US jurisdiction are required to report and respond to IRS summons. The idea that crypto is untraceable has been outdated for years — the Silk Road takedown in 2013 was largely a blockchain forensics exercise.

What crypto transactions are completely tax-free?

Buying with fiat currency, transferring between wallets you own, holding without selling, gifting within the annual gift tax exclusion ($19,000 per recipient in 2025), and donating to qualified charities. Receiving crypto as a gift is also not a taxable event at the time of receipt — but when you later sell it, you inherit the donor’s cost basis.

What’s the deadline to file crypto taxes for the 2025 tax year?

April 15, 2026. If you need more time, file Form 4868 by April 15 for an automatic six-month extension to October 15, 2026. The extension covers the filing deadline only — any taxes owed are still due April 15. Underpaying and filing late without extension triggers both failure-to-file and failure-to-pay penalties simultaneously.

This article is for informational purposes only and doesn’t constitute tax advice. Consult a qualified CPA or tax attorney for advice specific to your situation.

Our Review Methodology

We evaluate each post based on thorough research, credibility of sources, accuracy of information, and relevance to our readers. Our editorial team follows strict guidelines to ensure all content meets high standards of quality.

Disclaimer

The content in this article is provided for informational purposes only and does not constitute financial, investment, or professional advice. Always do your own research before making any decisions.