You made ₹40,000 flipping SOL tokens last November. Then you discovered you owe ₹12,480 of it to the government — and you can’t offset that against the ₹8,000 loss you took on a DeFi position in August. That’s India’s crypto tax system. No averaging, no loss carryover, no holding period discount. Just a flat 30% on every profitable trade, regardless of when you bought or what else happened in your portfolio that year.

India has 119 million active crypto users as of 2025 — the largest user base in the world (Disruption Banking, 2025) — and the Income Tax Department is paying close attention. In 2024-25, the Central Board of Direct Taxes sent over 44,000 compliance communications to taxpayers flagged for undisclosed crypto holdings. The enforcement machinery is running.

The Ministry of Finance confirmed in Parliament (February 2026): “Crypto is still unregulated, but under tax and enforcement radar.” That’s not ambiguous.

This guide breaks down everything you need to stay compliant in FY 2025-26.

India taxes crypto profits at 30% flat rate + 4% Health and Education Cess (effective 31.2%) under Section 115BBH. A 1% TDS applies to transactions above ₹10,000. Losses cannot be offset. File using Schedule VDA in ITR-2 or ITR-3 by July 31. Budget 2026 added ₹200/day and ₹50,000 penalties for non-reporting — the 30% rate itself is unchanged. (Income Tax Act)

What Is the Crypto Tax Rate in India?

India charges a flat 30% tax on all Virtual Digital Asset (VDA) profits plus a 4% Health and Education Cess, bringing the effective rate to 31.2%. This has been in force since April 1, 2022, under Section 115BBH of the Income Tax Act. No differentiation by asset type, no discount for long-term holding, no special treatment for NFTs or DeFi income. Bitcoin, Solana, a governance token from a two-week-old protocol — taxed identically.

The rate has two rules that make it notably harsher than standard capital gains tax:

Only deductible expense: cost of acquisition. Exchange fees, gas costs, wallet charges — none of these are deductible. Tax is calculated on sale price minus what you originally paid for the asset, full stop.

No loss offsetting. A profitable BTC trade cannot be reduced by an ETH loss in the same year. Each trade stands alone. You can’t offset crypto losses against salary income or any other income head either.

Quick illustration: buy 1 ETH at ₹2,00,000, sell at ₹2,80,000. Profit = ₹80,000. Tax = ₹24,000 + ₹960 cess = ₹24,960. The ₹15,000 loss you took on SOL the same week doesn’t factor in.

Is Crypto Taxed as Capital Gains or Business Income?

Neither, technically. The government deliberately avoided classifying VDAs as capital gains (which would invite holding period discounts and indexation benefits) or business income (which allows expense deductions). VDAs sit in their own category under Section 115BBH — taxed at the same flat rate as lottery winnings. Whether you held for a day or four years, your liability is identical.

For salaried individuals who also trade crypto, VDA income is a separate head assessed at 30%, regardless of your income slab.

Which Crypto Transactions Are Taxable?

Most active crypto use triggers tax. The CBDT’s position is clear: if you received value from a crypto asset in any form, it’s a taxable event. That includes crypto-to-crypto swaps at fair market value — which surprises traders who assume the tax trigger only comes from converting to INR.

| Transaction Type | Tax Trigger | Rate |

|---|---|---|

| Sell crypto for INR | Realized profit | 30% + 4% cess |

| Crypto-to-crypto swap | Fair market value of received asset | 30% + 4% cess |

| NFT purchase (using crypto) | Treated as crypto sale | 30% + 4% cess |

| NFT sale | Profit over cost | 30% + 4% cess |

| Staking rewards received | On receipt at fair market value | 30% + 4% cess |

| Mining rewards received | On receipt at fair market value | 30% + 4% cess |

| Airdrop received | On receipt at fair market value | 30% + 4% cess |

| DeFi yield | On receipt at fair market value | 30% + 4% cess |

| Crypto gift over ₹50,000 (non-relative) | On full value received | 30% + 4% cess |

| Salary paid in crypto | Standard income slab rates | Per slab |

Staking and mining deserve a specific note. When you receive rewards, that’s taxable event one — you’re assessed on the fair market value of the tokens that day. When you later sell those same rewards, the appreciation from your receipt-day cost basis is taxable event two. Two separate calculations for the same asset.

How Are Crypto-to-Crypto Swaps Taxed?

Swapping ETH for SOL is a taxable event on the ETH side. The ITD treats it as: you sold ETH at its current market value in INR, then bought SOL at that same value. Your profit on the ETH — from your original acquisition price to the day’s market rate — is taxable at 30% + cess immediately. You can’t defer until the SOL is eventually sold.

I learned this the uncomfortable way. During a DeFi-heavy period in 2021, I’d made around 40 token swaps — ETH to USDC, USDC to governance tokens, back to ETH. I hadn’t treated each one as a “sale.” When I sat down to properly calculate the tax position using FIFO and realized the cumulative liability, the number was genuinely uncomfortable. India was already treating swaps as taxable events even before Section 115BBH formally took effect. Keep a record of every swap, including the INR value at time of transaction. Every one. For MetaMask and other self-custody wallet users doing DeFi interactions, every on-chain swap is a potential taxable event. Most traders badly underestimate the cumulative position until they actually add it up.

Which Crypto Events Are Actually Tax-Free?

Three specific events are genuinely free from tax. Not “probably fine” — actually exempt.

Buying crypto with INR. Purchasing Bitcoin or any VDA with Indian rupees isn’t taxable. No profit has been realized. You’re converting one asset to another, and that conversion alone doesn’t create a taxable event.

HODLing. Unrealized gains are not taxable. Your portfolio doubled and you haven’t sold? Zero liability. India taxes realized profits only. Sitting on appreciation creates no obligation until you exit.

Transferring between your own wallets. Moving crypto from WazirX to your Trust Wallet, or between any two accounts you beneficially own, isn’t a taxable event. The cost basis carries over intact.

Here’s the catch, though. You need to be able to prove both wallets belong to you. The ITD may treat an unverified transfer as a sale. Download transaction histories from both sides, cross-reference addresses, and keep documentation showing same-owner control. If you’ve moved assets between a CEX and a DeFi wallet without records, reconstruct what you can now — before a notice arrives.

The gift exemption works like this: crypto received from a relative (as defined in the Income Tax Act) is tax-free. From non-relatives, gifts up to ₹50,000 in aggregate per year are exempt. Above that threshold, the full amount received becomes taxable income — not just the excess over ₹50,000.

How Does the 1% TDS on Crypto Work?

Under Section 194S (effective July 1, 2022), a 1% Tax Deducted at Source applies to crypto transactions above ₹10,000 per year for most traders, or ₹50,000 for “specified persons” — small traders and Hindu Undivided Families with turnover below prescribed limits.

TDS isn’t a final tax. It’s an advance payment on your annual liability. When you file your ITR, the TDS already deducted shows in Form 26AS and your Annual Information Statement (AIS) as a credit against total crypto tax due. If you’ve been over-deducted, you get a refund.

Who deducts it depends on how you trade:

- Indian centralized exchanges (CoinDCX, WazirX, Mudrex): The exchange handles TDS deduction automatically. You don’t need to do anything beyond filing.

- Peer-to-peer trades: The buyer is legally responsible for deducting TDS before paying the seller.

- Offshore exchanges (Binance, OKX, KuCoin): No automatic deduction. You’re responsible for self-reporting and depositing TDS.

That third category is where most of the 44,000+ CBDT notices originated. Indian banks flag crypto-related INR transfers. The ITD cross-references those against ITR filings. Trading on offshore exchanges without declaring means the transaction data exists in the banking system — it just isn’t in your Schedule VDA. And from April 2027, the OECD Crypto-Asset Reporting Framework means 52 participating nations will automatically share data on Indian residents’ crypto holdings.

Getting a TDS Refund

If TDS deducted across the year exceeds your actual crypto tax liability — common for high-volume, low-margin traders — you can claim the excess back. File your ITR accurately, declare TDS credits in Schedule VDA, and the refund processes through the normal ITD cycle. Worth doing; the amounts can be significant for active traders.

How to Calculate Your Crypto Tax

The formula is straightforward. Getting the underlying data together is where most traders get stuck.

The calculation:

Taxable profit = Sale proceeds − Cost of Acquisition

Tax payable = Taxable profit × 30% + 4% Cess

India uses a transaction-by-transaction method. Each sale is calculated independently. No netting of gains and losses across different trades within the same year.

Cost basis method: FIFO only. India accepts First-In-First-Out for VDA calculations. When you sell, the cost of your earliest-acquired units of that asset applies first. HIFO (highest-in-first-out) and weighted average cost are not accepted.

Worked example — two tranches of BTC:

You buy 0.5 BTC across two purchases:

- January 2025: 0.25 BTC at ₹15,00,000 per BTC (cost: ₹3,75,000)

- March 2025: 0.25 BTC at ₹20,00,000 per BTC (cost: ₹5,00,000)

In June, you sell 0.25 BTC at ₹22,00,000 per BTC (proceeds: ₹5,50,000).

FIFO means the January tranche is sold first. Cost basis: ₹3,75,000. Profit: ₹5,50,000 − ₹3,75,000 = ₹1,75,000. Tax: ₹1,75,000 × 30% = ₹52,500 + 4% cess = ₹54,600.

The ₹2,00,000 loss you took on a token position in April? Irrelevant to this calculation. Cannot be applied.

What you cannot deduct: Exchange transaction fees, gas costs, TDS already paid. Only the actual INR paid to acquire the asset qualifies as cost of acquisition.

How to Pay Crypto Tax in India

First question: do you need to pay advance tax? If your total crypto tax liability for FY 2025-26 exceeds ₹10,000, you’re required to pay in installments throughout the year rather than in one shot at filing time. Missing the installment dates triggers interest at 1% per month under Sections 234B and 234C.

Advance tax schedule (FY 2025-26, AY 2026-27):

| Installment | Due Date | Cumulative % of Annual Liability |

|---|---|---|

| 1st | June 15, 2025 | 15% |

| 2nd | September 15, 2025 | 45% |

| 3rd | December 15, 2025 | 75% |

| 4th | March 15, 2026 | 100% |

Which ITR form applies:

- ITR-2: Salaried individuals and those with investment income but no business income. Covers most casual crypto traders.

- ITR-3: Self-employed, professionals, or those whose crypto trading volume and frequency qualifies as business income. High-frequency traders are sometimes reclassified by the ITD as business income earners — if that applies to you, ITR-3 is required.

Schedule VDA is mandatory in both. You need to list each VDA transaction: acquisition date, sale date, cost of acquisition, sale proceeds, and resulting profit.

Step-by-step filing process:

- Download trade history from every exchange you used that year — most Indian platforms offer CSV exports

- For offshore exchanges, reconstruct INR values using historical price data (CoinGecko provides INR price history)

- Calculate profit per transaction using FIFO cost basis

- Aggregate TDS credits from Form 26AS and AIS

- Fill Schedule VDA with all transactions (the ITR portal computes your total liability from entries)

- Pay any remaining tax via Challan 280 through the income tax e-filing portal

- Submit ITR-2 or ITR-3 by July 31, 2026 for FY 2025-26 (AY 2026-27)

Third-party aggregators like KoinX and Koinly integrate directly with WazirX, CoinDCX, and most offshore exchanges to automate Steps 1 through 3. Worth using if you had more than 50 transactions.

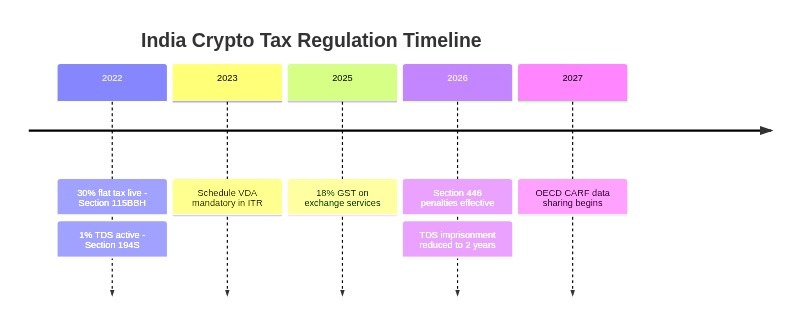

Budget 2026 and Recent Regulatory Changes

The 30% rate stayed unchanged in Budget 2026. So did the 1% TDS. What the budget added was sharper penalties and tighter reporting obligations — the government’s signal that it’s done waiting for voluntary compliance.

Section 446 — New reporting penalties (effective April 1, 2026):

- ₹200 per day for late filing of required crypto information with tax authorities

- ₹50,000 flat fine for filing inaccurate crypto information

These apply to crypto exchanges (which have mandatory reporting obligations) and to individual taxpayers who fail to disclose VDA holdings correctly in their ITR.

Section 158B — Undisclosed VDAs: Crypto holdings discovered during an income tax search that weren’t declared in your ITR are taxed at 60% — not the standard 30%. That’s the “undisclosed income” rate. No deductions. If the ITD finds crypto balances during a search that don’t appear in your returns, expect a 60% assessment plus potential prosecution.

Section 276B amendment: Maximum imprisonment for TDS defaults reduced from 7 years to 2 years. The government is treating TDS as a compliance mechanism rather than a criminal enforcement tool. Fines and civil penalties remain significant.

18% GST on crypto exchange services (July 7, 2025): Trading fees, withdrawal fees, and other exchange services now attract 18% GST. This is on the platform’s fee, not the transaction value itself. On a ₹200 trading fee: ₹36 in GST. Active traders with ₹2,000–5,000/month in fees feel this materially over the year.

OECD CARF from April 2027: India joined the Crypto-Asset Reporting Framework alongside 52 countries. From April 2027, CARF-participating exchanges automatically report Indian residents’ crypto holdings to Indian tax authorities. That includes Coinbase, Kraken, and others. If you’ve been trading offshore without declaring, the compliance window is narrowing.

Fair warning:

CARF’s retroactive reach is being underestimated. Participating exchanges are already building reporting infrastructure. The data submitted from April 2027 will likely cover full account history — not just activity from that date forward. If you’ve held balances on offshore platforms without declaring, get ahead of this before 2027. Voluntary disclosure now is significantly better than a CARF-triggered assessment later. Crypto Tax for NRIs: Key Rules

India taxes NRIs on income that arises or accrues in India. For crypto specifically: trading on Indian exchanges or holding VDAs on Indian-registered platforms creates Indian-source income, and the 30% + 4% cess applies.

Residential status and tax scope:

| Status | Crypto Income Taxable in India |

|---|---|

| Resident Indian | All global crypto income |

| NRI | India-sourced income only |

| RNOR (Resident but Not Ordinarily Resident) | India-sourced + foreign income remitted to India |

DTAA applicability. India has Double Taxation Avoidance Agreements with over 90 countries. If you’re resident in a DTAA country, you may be able to claim credit for foreign taxes paid against your Indian liability. The problem: Section 115BBH sits outside the standard capital gains category, which makes DTAA mapping technically complicated. Claiming DTAA relief on crypto income without proper analysis can backfire. Get professional advice before applying it.

Offshore exchange holdings. Indian residents (including NRIs who’ve returned and re-established residency) must disclose foreign assets — including crypto on foreign exchanges — in Schedule FA of their ITR. With CARF from 2027, the ITD will have independent access to this data. Voluntary disclosure in Schedule FA is the preferable path.

What Are the Penalties for Not Paying Crypto Tax?

CBDT has moved from monitoring to enforcement. The 44,000+ compliance communications in 2024-25 weren’t warning shots — many resulted in formal assessments. Here’s the penalty structure:

Civil penalties:

| Violation | Consequence |

|---|---|

| Under-reporting income | 50% of additional tax due |

| Misreporting income | 200% of additional tax due |

| Late payment interest | 1% per month (Sections 234A, 234B, 234C) |

| Late crypto information filing (post April 2026) | ₹200 per day |

| Inaccurate crypto information filing (post April 2026) | ₹50,000 flat fine |

| Undisclosed VDA found during search (Section 158B) | 60% tax on discovered amount |

Criminal liability:

Willful tax evasion carries up to 7 years imprisonment. TDS default: up to 2 years (reduced from 7 years in Budget 2026).

The P2P-specific risk. INR transfers made for P2P crypto trades look identical to unexplained cash credits in the ITD’s screening system. CBDT has specifically flagged P2P transactions on Binance P2P and similar platforms. In some early-2025 notices, the effective penalty rate reached 78% of transaction amounts: 30% tax on the full transaction value (when the source is “unexplained”) plus a 50% misreporting penalty plus interest. This isn’t theoretical — Indian traders received these assessments for FY 2021-22 P2P activity.

The Bottom Line on Crypto Tax in India

India’s 31.2% effective rate is among the highest globally for crypto. It doesn’t allow loss offsets, doesn’t reward holding period, and the enforcement infrastructure is getting more capable every year. OECD CARF from 2027 means offshore trading won’t stay invisible. If you’re active in the Indian market, the question isn’t whether the ITD will eventually find discrepancies — it’s whether you’ve given them a reason to act on them.

The practical reality: the filing process is manageable. Indian exchanges provide trade history exports. Schedule VDA in ITR-2 is well-documented and the portal walks you through it. The 1% TDS already creates a partial paper trail the ITD can cross-reference. Working with that structure — not against it — is the rational path.

For a review of which Indian exchanges offer the best trade history exports and compliance reporting, see our Best Crypto Exchanges guide. If you’re moving to self-custody and need a wallet that works well for Indian DeFi users, our Trust Wallet review and MetaMask review are good starting points.

Frequently Asked Questions

Is crypto legal in India? Yes — crypto isn’t banned in India. Trading, holding, and transacting are all permitted. It’s unregulated as a financial product but fully subject to income tax. See our guide on whether cryptocurrency is legal in India for the full regulatory picture.

Can I offset crypto losses against other income in India? No. Section 115BBH explicitly prevents offsetting crypto losses against crypto gains, capital gains from other assets, or any other income. Each profitable trade is assessed individually. Losses don’t carry forward to future assessment years.

Which ITR form should I use for crypto income? ITR-2 for salaried individuals and those with investment income but no business income. ITR-3 if you have business or professional income, or if your crypto trading qualifies as business income. Both require Schedule VDA.

What is Schedule VDA and how do I fill it? Schedule VDA is the dedicated crypto reporting section added to ITR-2 and ITR-3 from AY 2023-24. For each VDA transaction, you enter: acquisition date, sale date, cost of acquisition, sale price, and profit. The ITR e-filing portal calculates your total tax liability from these entries.

Do I pay tax when I transfer crypto between my own wallets? No — a transfer between wallets you beneficially own isn’t a taxable event because you haven’t sold anything. The cost basis carries over unchanged. Keep documentation proving both wallets belong to you. Without that, the ITD may treat the transfer as a sale.

When is the deadline to file crypto taxes for FY 2025-26? July 31, 2026 (Assessment Year 2026-27) for individuals not subject to audit requirements. If your total tax liability exceeds ₹10,000, you’re also required to pay advance tax in four installments throughout the year — missing those triggers interest charges.

Will India reduce the 30% crypto tax rate? Nothing confirmed as of April 2026. The crypto industry has repeatedly lobbied for a lower rate and loss-offset provisions. Budget 2026 made no movement on either. The government’s current trajectory is toward tighter enforcement of the existing rules, not rate reduction.

What is the 60% tax under Section 158B? Section 158B applies when the ITD discovers undisclosed VDA holdings during a formal search or inquiry. Crypto that wasn’t declared in your ITR is classified as “undisclosed income” and taxed at 60% — double the standard 30% rate. No deductions are available, and prosecution may follow depending on the amount involved.

This article is for informational purposes only and does not constitute tax or financial advice. India’s crypto tax rules are complex and subject to change. Consult a qualified chartered accountant for advice specific to your situation.

Our Review Methodology

We evaluate each post based on thorough research, credibility of sources, accuracy of information, and relevance to our readers. Our editorial team follows strict guidelines to ensure all content meets high standards of quality.

Disclaimer

The content in this article is provided for informational purposes only and does not constitute financial, investment, or professional advice. Always do your own research before making any decisions.